By Nick Farnell

For decades, the RV industry has relied heavily on seasonal intuition, historical norms, and local lot trends to manage inventory. The unprecedented retail surge of 2021 and 2022, followed by a broader economic cooldown, has fundamentally reshaped the secondary market. Today, dealerships are facing a highly concentrated model-year over supply, distinct geographic inventory pockets, and widening price variances that “gut-feel” appraisals simply cannot account for.

To survive and protect margins in this current landscape, dealerships must look beyond their own lots. By analyzing the physical composition, age, and pricing characteristics of the national pre-owned market, dealers can leverage macro-data to make highly profitable micro-decisions.

Market Composition: What’s Actually on the Lot?

To understand current pricing dynamics, we must first look at the physical makeup of Canada’s pre-owned inventory. The data reveals a market heavily concentrated by both unit type and geography.

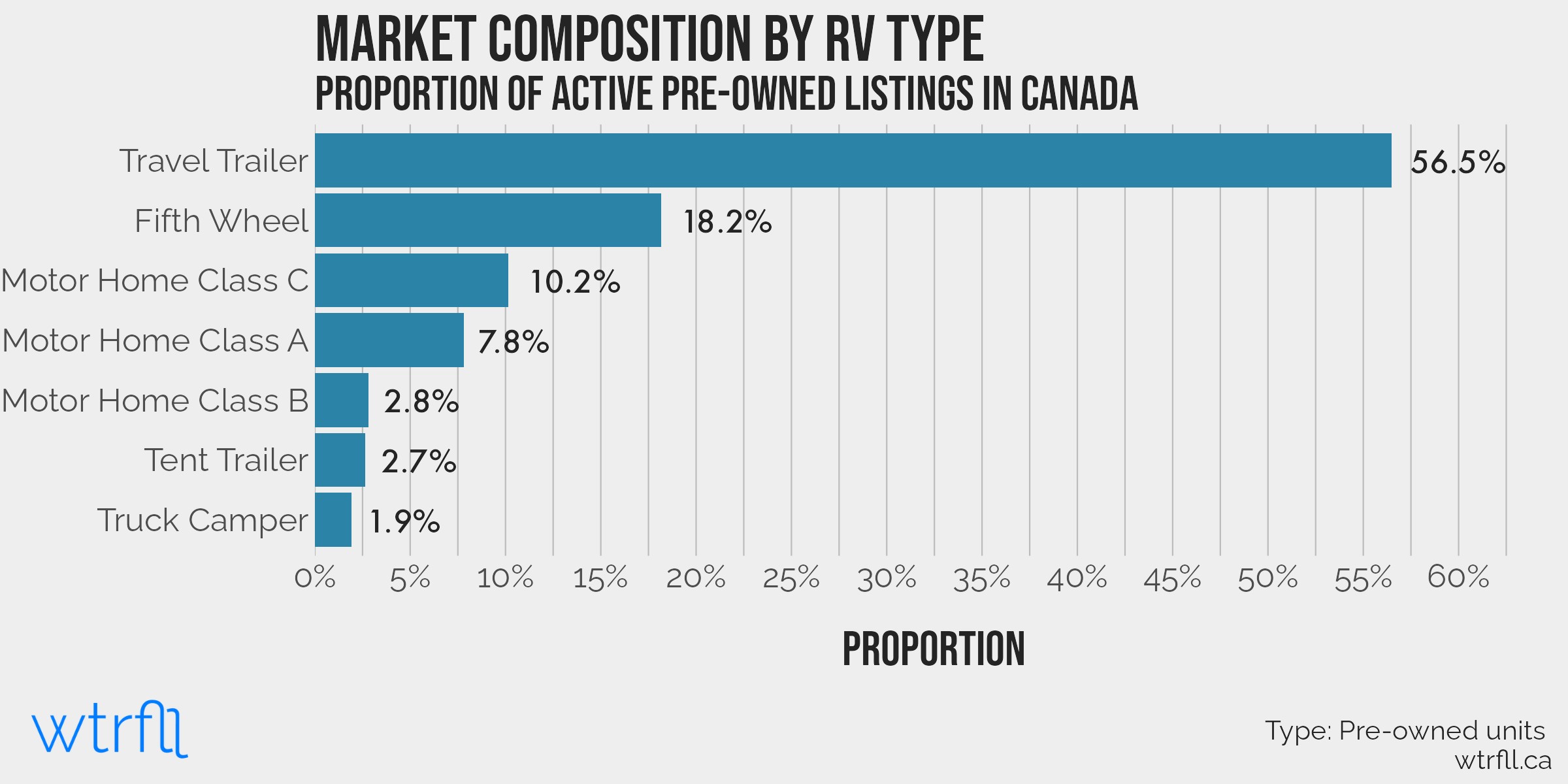

The Towable vs. Motorized Divide A macro-level view of active listings in Canada shows that towable units absolutely dominate the secondary market, representing approximately 80% of all available pre-owned inventory.

- Travel Trailers are the undisputed majority, making up more than 55% of all listings.

- Fifth Wheels represent the second-largest category at 18%.

- Tent Trailers (3%) and Truck Campers (2%) make up a negligible fraction of the towable market.

Motorized units represent the remaining listings. Within this segment, Class C motorhomes are the most readily available (10%), followed by Class A (8%) and the much scarcer Class B camper vans (3%).

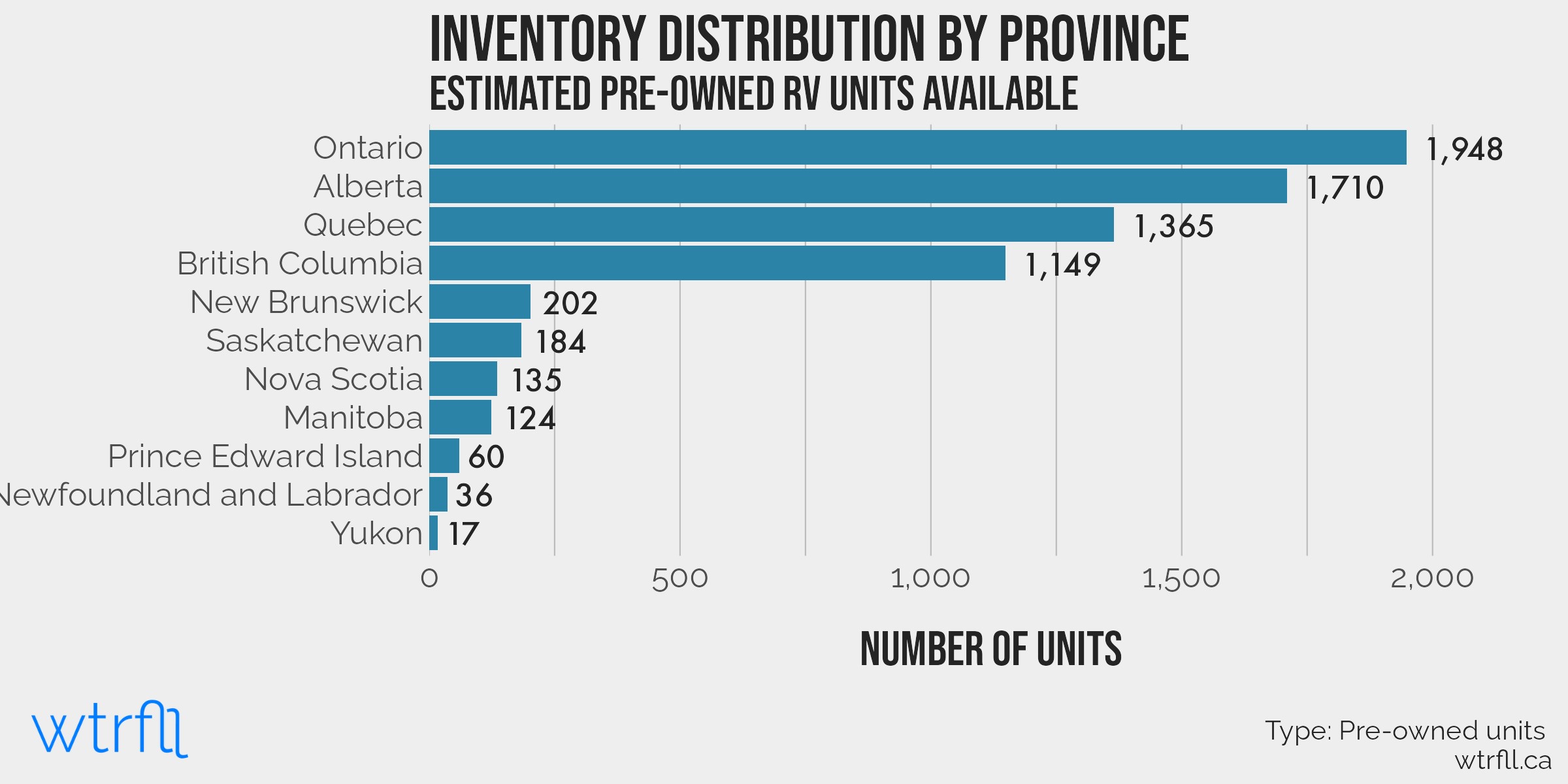

Provincial Concentration Inventory is not distributed evenly across the country. The secondary market is heavily anchored by four specific provinces, which together hold the vast majority of Canada’s pre-owned RVs:

- Ontario leads the nation with 1,948 active units.

- Alberta follows closely with 1,710 units.

- Quebec (1,365) and British Columbia (1,149) round out the “Big Four.”

Floorplan Trends When drilling down into specific floorplans, clear patterns emerge. In the towable categories, standard high-volume bunkhouses and popular couples’ coaches (such as the Jayco Jay Flight 174BH) represent the highest density of listings.

The Age of the Fleet: Navigating the 2022 Oversupply

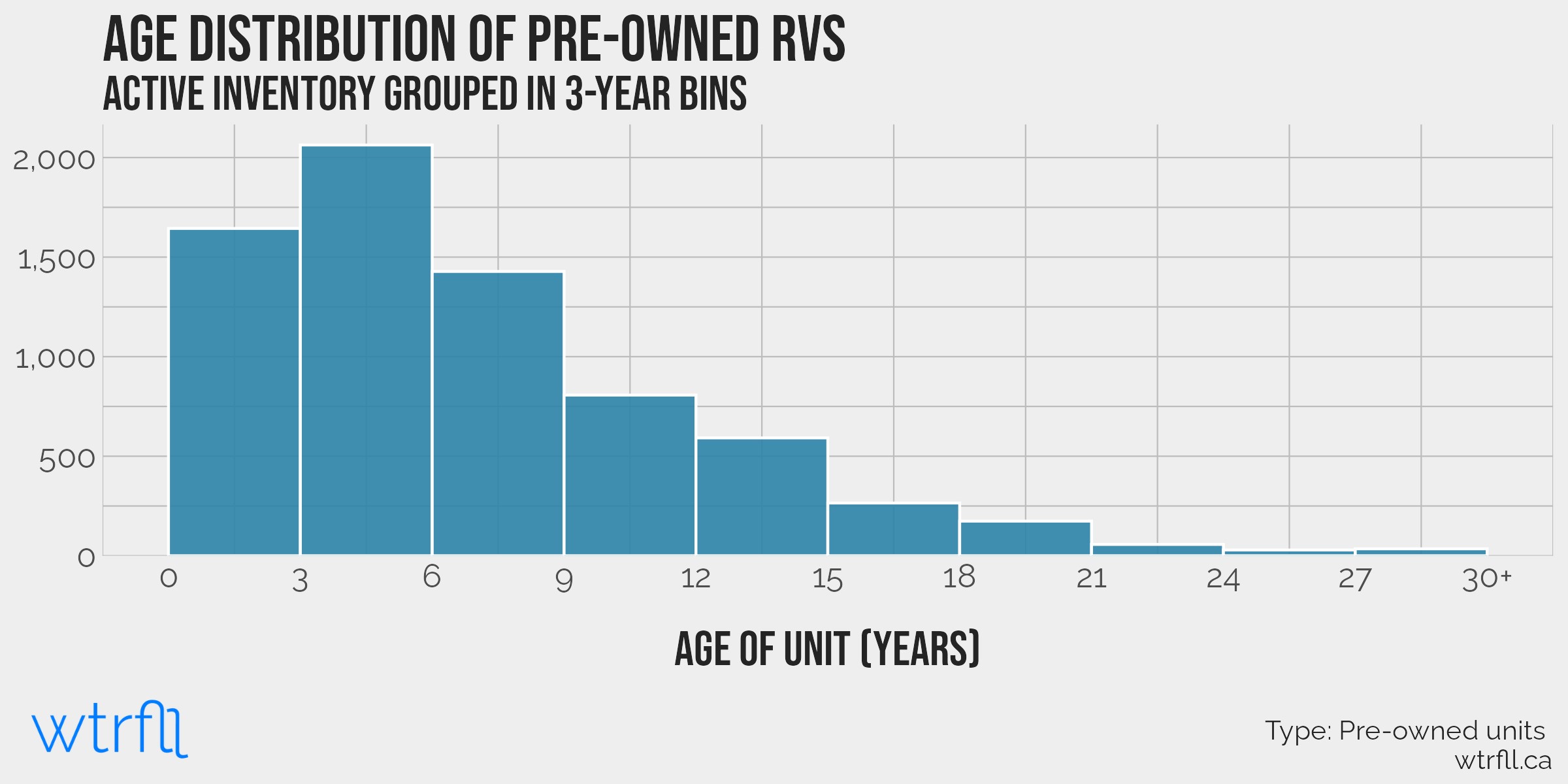

Turning to the chronological age of active inventory, the data reveals a market distinctly skewed toward newer units. Rather than an even spread across decades, the national fleet is heavily concentrated in the late-model and mid-life brackets.

The 3-to-6-Year Spike The pre-owned market is dominated by RVs under a decade old. The absolute highest volume of available inventory sits squarely within the 3-to-6-year bracket, peaking at over 2,000 active listings nationwide. Once a unit passes the 12-year mark, overall market availability drops off quickly.

The Pandemic-Era Anomaly When transitioning from grouped age brackets to specific model years, the most critical data point of the year emerges. Currently, the 2022 model year makes up nearly 16% of all available pre-owned listings nationwide, flanked by disproportionately high volumes of 2023 and 2021 models.

Objectively, this suggests the entry of pandemic-era purchases into the secondary market. The historic wave of consumers who bought new RVs during the peak of the boom have now reached a common three-to-five-year ownership milestone. This cohort is actively cycling back into the market via trade-ins and private sales, creating a highly concentrated glut of inventory centered directly on the 2022 model year.

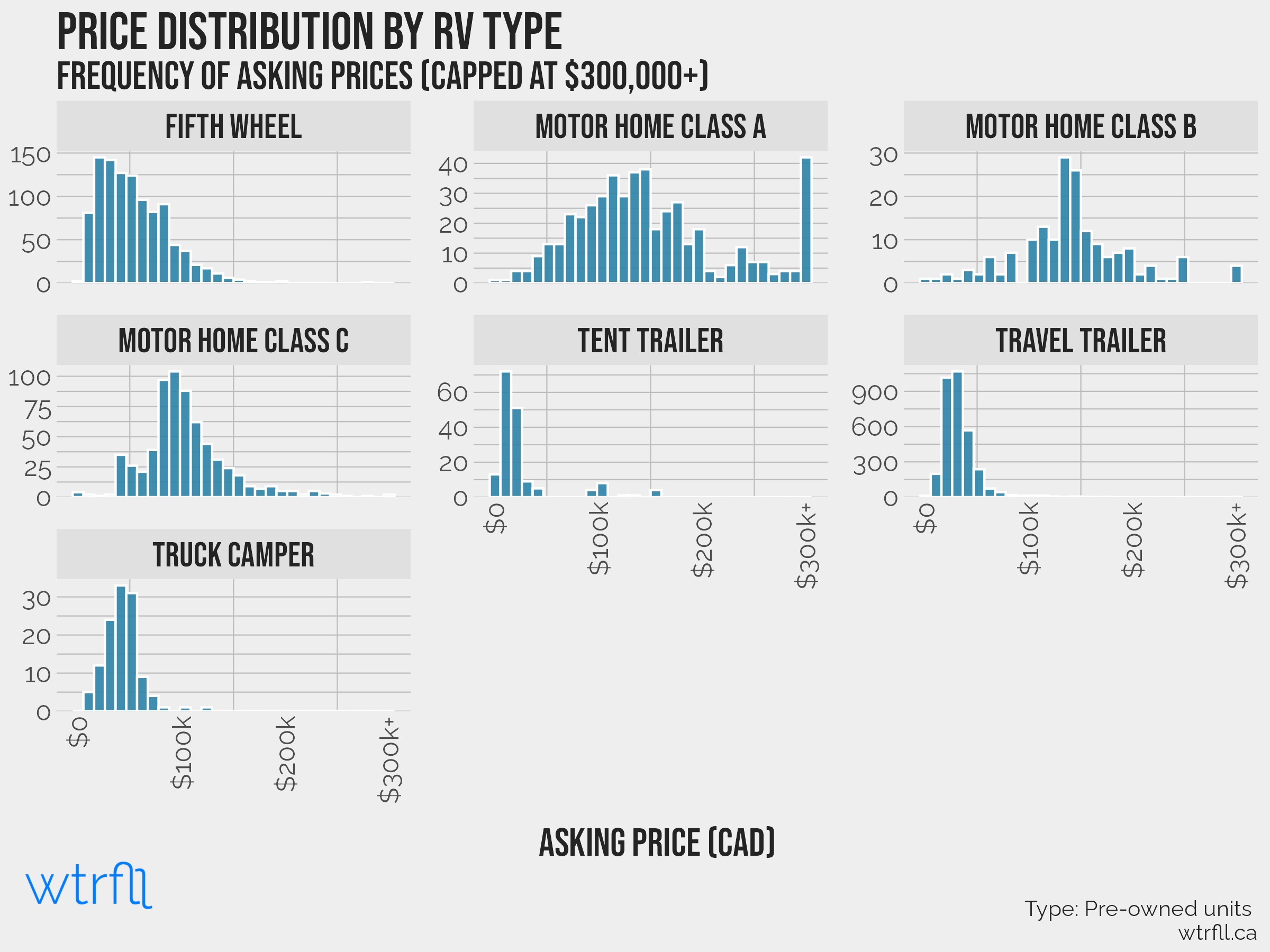

Pricing Characteristics: The Cost of Guessing

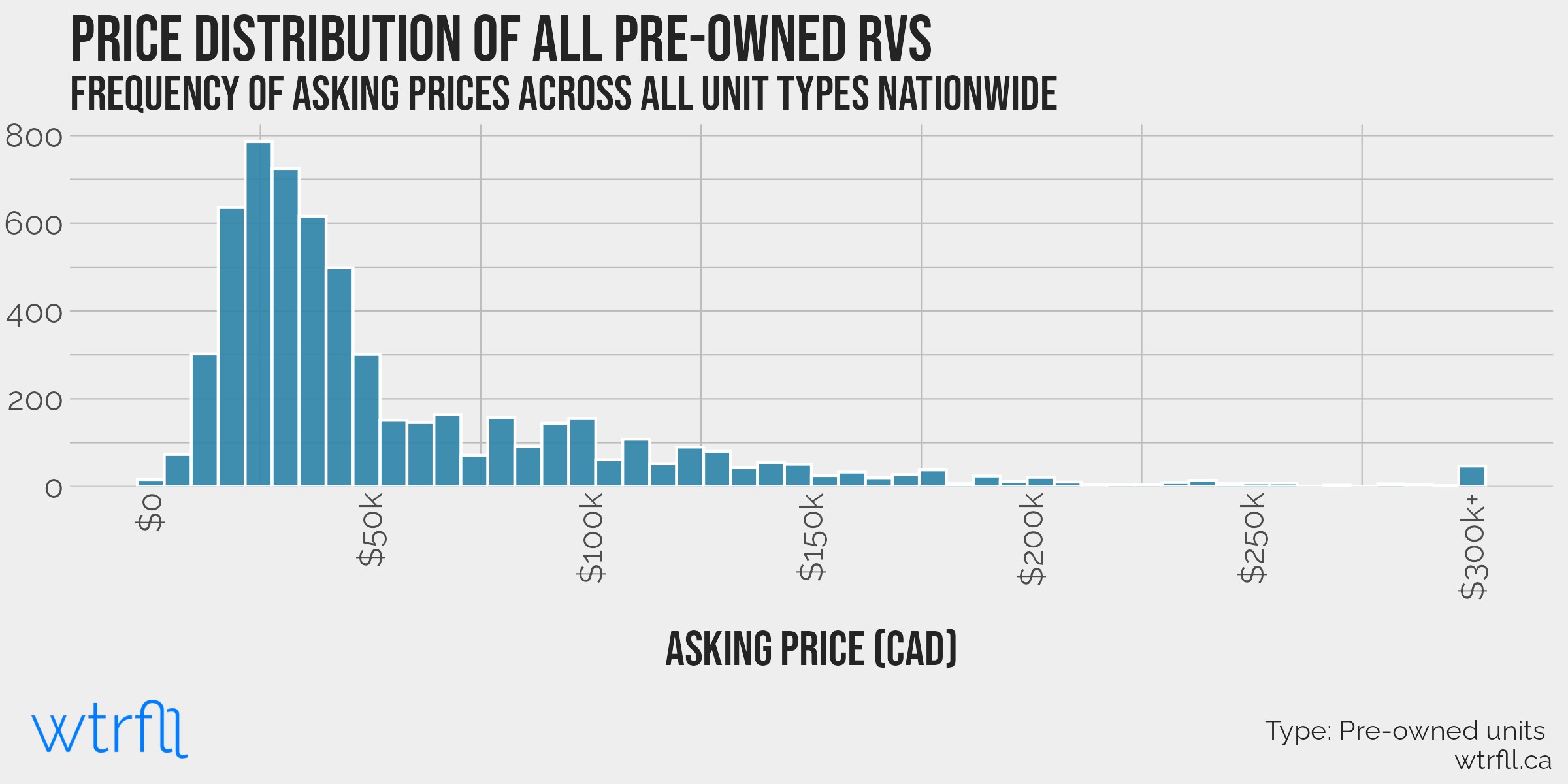

As we transition from chronological age to dollar values, the national inventory displays a high degree of pricing sensitivity. While luxury diesel pushers often capture the headlines, the actual volume of the pre-owned market is concentrated in a much tighter financial bracket.

The $25,000 to $45,000 Sweet Spot The market is heavily weighted toward the entry and mid-level segments. The largest cluster of pre-owned inventory is priced between $25,000 and $45,000 CAD, with the absolute peak frequency occurring just before the $35,000 mark. Units priced above $100,000 see a drastic drop-off in volume.

When breaking this down by class:

- Travel Trailers display the tightest grouping, with a massive spike in availability under $40,000.

- Class A Motorhomes display a wide “Bell Curve” shifted to the right, maintaining a strong presence even in the $300,000+ brackets.

- Tent Trailers & Truck Campers live almost entirely under the $25,000 and $50,000 marks, respectively.

The Cost of Guessing: Variance in the Field Likely the most critical takeaway for a dealership’s appraisal desk is the sheer variance found within seemingly identical categories. A “Class C Motorhome” is not a monolith; age, brand, and condition create massive spreads that intuitive pricing cannot safely navigate.

For example, when looking at 5-year-old units (2021 Class C Motorhomes), the data shows the “cost of guessing” in real-time. Across Canada, the asking price for this specific year and type can easily range by tens of thousands of dollars.

The Data-Driven Dealership

The pre-owned RV market is no longer a landscape where dealerships can afford to appraise inventory by checking the wind. With a massive influx of 2022 model-year trade-ins currently flooding the market and massive pricing variances confusing consumers and dealers alike, a systematic approach is required.

This data proves that without a solid baseline, dealers risk pricing themselves out of a competitive local market, or worse, leaving tens of thousands of dollars in margin on the table. By treating the lot as a portfolio of data points rather than just a collection of used units, modern dealerships can navigate the post-pandemic correction and identify the hidden margins that keep the business thriving.

Nick Farnell is a professor of business analytics and runs the consulting firm wtrfll, focusing primarily on competitive intelligence and data driven insights. When not in front of a computer, he is spending as much time as possible in one of Ontario’s provincial parks with his young family.

Please visit https://wtrfll.ca/ to see how Nick and his team have helped organizations use data and analytics to better understand their customers and competitors.